The 2007 crisis reignited the debate on the growth of inequality. Only major institutional changes, like those proposed by Thomas Piketty, can halt the trend of increasing income and wealth disparities. But how precisely has inequality evolved from 2007 to 2014?

In the Wake of the Crisis

In the developed world, the immediate effect of the 2007 economic crisis was less inequality. 2008 and 2009 saw a decline in the percentage of income retained by the wealthiest households. The scope of this decline varied by country. In English-speaking countries and certain European nations, such as France, Ireland, and Denmark, the income of the top 1% fell by about 10% from 2007 to 2009. In Sweden, Japan, and, to a somewhat lesser degree, Italy and Spain, the drop was more moderate. This shift can be explained mostly by the volatility of capital gains—dividends, interest, rents, and surpluses—which carry so much weight for those at the top of the wealth distribution, compounded by capital losses. In fact, the reduced holdings of the wealthiest households can be explained by capital losses alone. In the United States, if we take out these cyclical components of income, we see no decline in inequality.

The compressed income distribution immediately following the crisis has been canceled out in the years since 2010. The economic recovery, though fragile, has been most beneficial for the most well-off. This is mainly due to the passage of time between the financial crisis itself and its present effects on the economy; it had a powerful and immediate effect on capital income, whereas the impact on unemployment, and consequentially the overall economy, took months and years to materialize, at which point capital income had had time to rebound. In the United States, like in France, inequality has returned to its pre-crisis level. Thus from 2009 to 2012, in the US, income growth for the top percentile was at 31.4%, while the other 99% saw their income stagnate, increasing only 0.4% during the same period. The top 1% thus captured 95% of the gains of the American economic recovery. A Federal Reserve study confirms this result, showing a widening gap between average and median pre-tax household income. From 2010 to 2013, median income fell by 5% while the average went up 4%. These opposing movements indicate growing inequality. Income distribution in the United Kingdom seems to have followed the same trend, because after a drop in 2009 and 2010, income inequality was on the rise again in 2011. The economic recovery seemed to have the least benefit for the wealthy in Australia and Canada, where inequality has never (yet) returned to pre-crisis levels. For Scandinavian countries such as Denmark and Sweden, the data indicate a reversion to the inequalities observed before the crisis, but these countries had more income parity in the first place. Metrics in Germany, Italy, and Japan are available only through 2009 or 2010, but the results suggest a similar growth of inequality.

The statistics on high income are of a fiscal nature. They provide information on taxable income, but by design they ignore the effects of taxes and public transfers. These two elements of household fiscal structure must be accounted for to evaluate a household’s standard of living. A 2014 study by the French National Institute for Statistics and Economic Research (INSEE) details the recent evolution of French living standards. Taken as a whole, the country’s median household standard of living remained steady between 2007 and 2012. However, this did not hold true for everyone. During the economic crisis, the lower deciles saw their standards of living decline while those of the upper strata were rising. The contrast between the lowest and highest parts of the income distribution automatically led to greater disparity in standards of living. So after remaining stable in 2008 and 2009, the Gini index of household living standards reached 0.306 in 2011 before stabilizing in 2012. The rise of inequality is confirmed by other indicators such as the ratio of overall standard of living to the progression of the poverty rate. In 2012, the wealthiest 20% had a living standard 4.6 times higher than that of the poorest 20% (compared to 4 times higher during the 1990s and 4.3 times higher in the years before the economic crisis). In France, the poverty rate reached13.5% in 2009 and 14.3% in 2011, and the depth of poverty, measured by the difference between the living standard of the poorest households and those at the poverty line, was markedly exacerbated in 2012. The system of social protections has not been enough to compensate for elevated inequality and poverty in the years since the recession. Nevertheless, without social and fiscal transfers, this elevation would have been even more prominent.

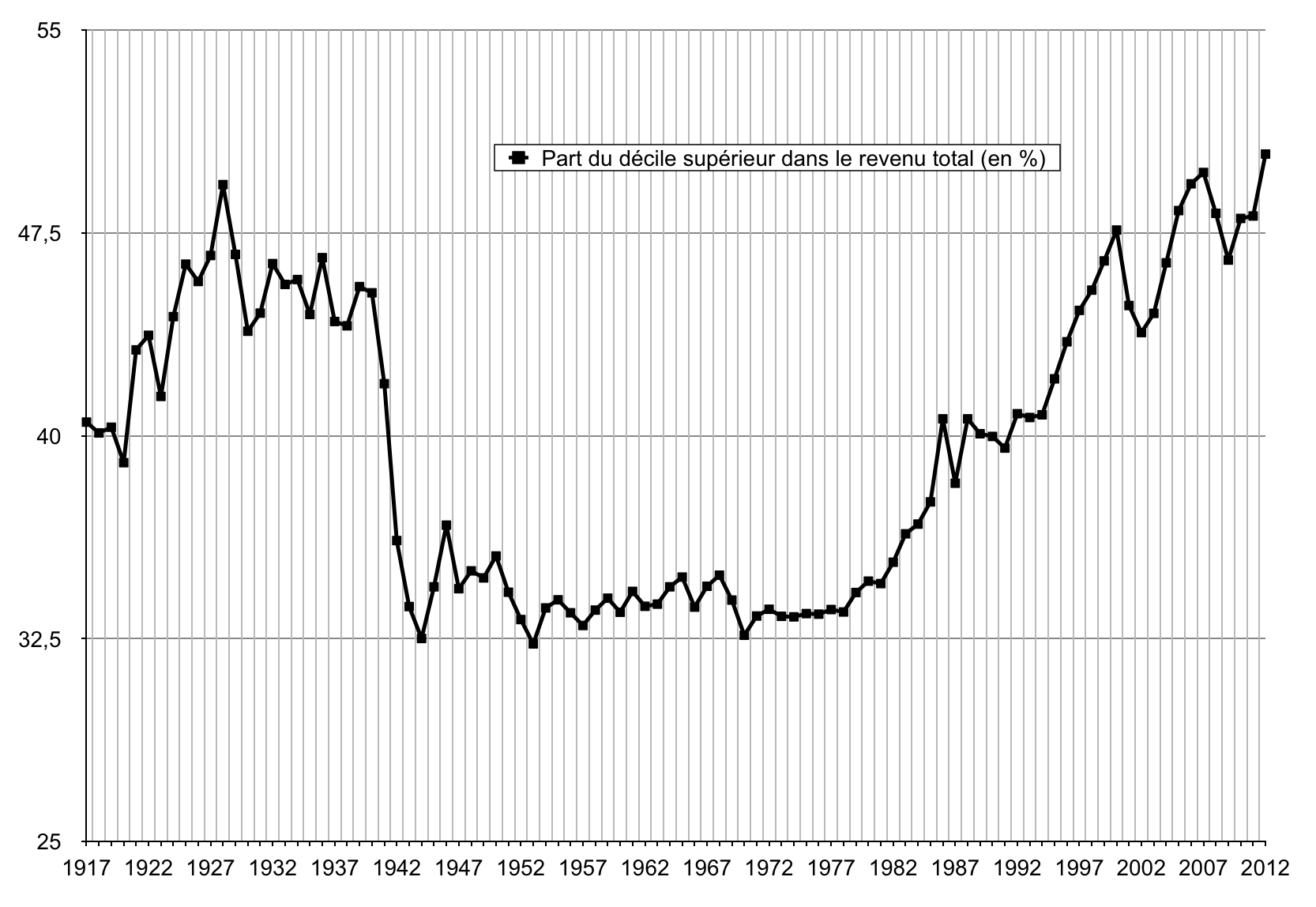

Inequality Growing Exponentially since the 1970s

To better understand the short-term trends around inequalities, it is essential to take a long-term view. Growing inequality is not a new phenomenon. In most developed countries, the end of the 1970s was the point of departure for a growing disparity in income and patrimony. In English-speaking countries, but also to a lesser degree in Western Europe and Japan, the 1970s marked the end of a half-century of declining or relatively stable inequality. It is nonetheless significant and interesting to note that the forms of these inequalities, and their timing, varied from one country to another.

The increasing disparity of income distribution has affected every developed nation to some degree, even in Scandinavia, the most historically egalitarian region.

In English-speaking countries, the scale of the increase is unequivocal. In the United States, since the late 1970s, almost 15 points of national income were transferred from the lower 90% of households to the wealthiest 10%. The United Kingdom and Canada saw a similar, though slightly more moderate, shift. In Europe and Japan, inequality was also up during the 1980s, but it grew in slower and smaller increments. The transfer of national income to the top 10% in Japan was around 10 points. For European countries, this transfer was usually “limited” to 5 points of national income, though there were differences between continental Europe (Germany, France, the Netherlands, and Switzerland) and southern or northern Europe; the continental countries experienced a more moderate rise in inequality. Still, even at the heart of these regions, differences remain. France was a notable exception, with inequality slightly decreasing in the 1970s and ’80s. Yet by the end of the 1990s income inequality was up, particularly at the top of the distribution. So from 1980 to 2010, income inequality in France resembled a U-curve. It’s important to note that the increasing disparity of income distribution has affected every developed nation to some degree, even in Scandinavia, the most historically egalitarian region.

The inequality trend has many causes, and they vary by country. Even if the distinctions are complex in reality, we can attempt to isolate the common factors across all countries (globalization, technological progress) from the country-specific factors (fiscal politics, labor market regulations, relative standards of executive compensation). An increasing distribution of income to the upper percentiles tends to indicate that technological progress, which should be beneficial to skilled workers, is not a sufficient explanation. Diminishingly progressive fiscal systems since the 1980s, as well as the influence of capital, seem to better correspond to observed realities. Though they are complex, the analysis and quantification of these different explanations are promising areas of research.

The Resurgence of Patrimony in Developed Nations

For a comprehensive analysis of income inequality, we must also consider the role of patrimony and the income it generates (interest, rents, dividends). This is crucial to our understanding not only of the effect of the economic crisis on inequality but also on the progression of inequality over time.

Analysis of income composition for the upper income strata indicates that capital gains are a significant component. For the richest 0.1%, capital gains are larger than earned income. The consequences of lost financial capital due to the crisis were correspondingly large for people in this category. Besides the income from patrimony, however, consider the patrimony itself. Piketty and Gabriel Zucman, estimating the ratio of private patrimony to national income from 1970 to 2010, found evidence of a resurgence of capital in most developed countries. There are notable differences between continental Europe and the English-speaking world. Among the countries studied, during the 1970s the ratio was in the range of 200% to 300%; today it ranges from 600% to 700% in continental Europe versus 400% in English-speaking countries. The central mechanism of this emerging capital, that is, the difference between the rate of economic growth and the rate of capital returns, indicates a return to levels observed in Europe at the end of the 19th century. When we look at patrimony, we can show that inequality takes different forms. Patrimony has a much heavier influence in continental Europe and Japan than in English-speaking countries, where wage inequality is more of a factor. Emmanuel Saez and Zucman have shown, however, a severe increase in patrimony inequality in the United States since the 1980s, especially at the top of the distribution, where the current holdings of the richest 0.1% are comparable to 1920 levels.

Accounting for patrimony allows for a more complete analysis of shifting inequality; we can see that the more moderate growth of income inequality in continental Europe than in English-speaking countries is counterbalanced by the stronger influence of patrimony. The nature of inequality is not identical for every wealthy country.

Economic Crisis, Political Response

Historically, the rise of inequality immediately after the 2007 crisis is not so surprising in light of past economic events. The crash of 1929 provides a clarifying example. Much like the current recession, the crash damaged income through depreciation and the reduction of capital gains. Nonetheless, the change in composition of income between 1929 and 2007 tends to indicate that the Great Depression probably had a more severe effect. In 1929, capital gains were higher than earned income for the wealthiest 1%. In 2007, this was true only for the wealthiest 0.1%. Contrary to popular belief, the Great Depression led to no lasting reduction of inequality in the developed world. Only the political responses brought to bear on this crisis have had the least effect on inequality of income and patrimony.

The politics in action after the 1929 crash, and more generally the institutional changes occurring in the 1930s and 1940s, had a marked and lasting impact on the distribution of wealth. In most developed countries, the highest marginal tax rate had jumped significantly in earlier years: in France, from 2% in 1915 to 72% in 1924. That rate fell until the start of the 1930s, when it reached a quasi-confiscatory level (almost 90%) especially in the US and UK, and stayed there until the 1980s. There was an appreciable difference in the political response following the 2007 crisis, as there were no higher taxes on the wealthy (or very few) to offset austerity measures.

If we want to effectively combat inequality today, we have to account for financial integration, creating a regional, if not global, tax system.

The 2007 crisis launched a debate on the role of inequality in triggering the collapse. Had rising inequality weakened the financial system? Many recent findings seem to answer in the affirmative. In particular, the growing gap in income and patrimony since the 1980s may have led people of modest means to go into debt in order to maintain their level of consumption. This is still up for debate, as inequality linked to exploding private debt is less evident in European countries, yet the financial crisis still trampled them. Moreover, economic history indicates that financial instability can also be caused by other factors. The effect of inequality and, by extension, of a tax system considered overly favorable to the wealthiest classes is consistent with the line of research led by Piketty and Saez, which aims to interrogate the existing models of optimal taxation. In their view, elevated taxes on income or patrimony can be implemented without creating disincentives to work and save money. If we want to effectively combat inequality today, we have to account for financial integration, creating a regional, if not global, tax system. This would require a census of patrimony at the global level and a fight against the financial opacity created by tax havens.

Considering that the crisis coincided with weaker support of the welfare system in France and a hardening of public opinion against social aid for poor households and the unemployed, transforming the taxation system is especially necessary. The situation is atypical, given that periods of rising poverty are usually accompanied by social and political support for the most unfortunate. Public mistrust is fueled by the sense that certain people profit from an unjust socioeconomic system. Without an appropriate political response, this economic crisis, which could have been revelatory, will ultimately have no bearing on the question of wealth distribution. Regardless of magnitude, an economic crisis has merely a temporary effect on the distribution of resources. Only major institutional changes can check the trend of growing inequality of income and patrimony.

Further reading

Bordo, M. et C Meissner, (2012), “Does Inequality Lead to a Financial Crisis?”, Journal of International Money and Finance, 31(8), pp. 2147-2161.

Bertrand, M. and A. Morse, (2013), “Trickle-down Consumption,”, NBER Working Paper No. 18883.

Kumhof M., R. Rancière et P. Winant (2013), “Inequality, Leverage and Crises”, Mimeo.

Piketty, T. et G. Zucman (2013), “Capital is Back: Wealth-Income Ratios in Rich Countries 1700-2010”, Mimeo.

INSEE (2013), “Inégalités de niveau de vie et pauvreté”, Vue d’Ensemble, pp. 9-29.

Landais C. (2009), “Top Incomes in France (1998-2006): Booming inequalities?”, PSE Working Paper.

Saez E. (2013), “Striking it Richer: The Evolution of Top Incomes in the United States”, Mimeo

Piketty T. (2003), “Income Inequality in France, 1901-1998”, Journal of Political Economy, vol. 111, no 5, p. 1004-1042.

Piketty T. et E. Saez (2003), “Income Inequality in the United States, 1913-1998”, Quarterly Journal of Economics, vol. 118, no 1, p. 1-39.

Piketty T. et E. Saez.(2013), “A Theory of Optimal Inheritance Taxation”, Econometrica, vol.81, n.5, 2013, p.1851-1886.

Piketty T. et E. Saez (2013), “Top Incomes and the Great Recession”, IMF Economic Review, vol.61, n.1, 2013, p.456-478.

Piketty T. et E. Saez et S. Stantcheva (2013) “Optimal Taxation of Top Labor Incomes: A Tale of Three Elasticites”, American Economic Journal: Economic Policy, 2013, forthcoming.

Rajan, R. (2010), Fault Lines, University of Chicago Press.