Japan’s experience over the past year is probably more similar to that of Germany, whose rapid economic downturn was caused by a precipitous decline in exports, than to that of the U.S. and Britain, which are the epicenters of the crisis. What can Japan’s experience during the last crisis teach about post-crisis?

The failure of corporate governance arrangements contributed to the Japanese banking crisis of 1997 and the subsequent economic slowdown. Some of these arrangements such as the main bank system and cross-shareholding – which have been viewed as important features of the Japanese economic system and as sources of Japanese competitiveness – have encouraged excessive investment by corporations during the bubble era of the late 1980s and helped to delay corporate restructuring following the banking crisis. Nonetheless, shortcomings in Japanese corporate governance practices were not a direct cause of the current financial crisis, which was triggered by the subprime loan problem as exogenous shocks. Japan’s experience over the past year is probably more similar to that of Germany, whose rapid economic downturn was caused by a precipitous decline in exports, than to that of the U.S. and Britain, which are the epicenters of the crisis.

On the contrary, however, the global financial crisis is expected to have a significant impact on the evolution of corporate governance. Japanese corporations had been moving forward with reforms against a backdrop of globalization and deregulation from the late 1990s, and corporate governance arrangements had been evolving into hybrid forms. Then, the current crisis has a major impact on how corporate governance will evolve in the future. In this essay, I will reflect on the possible nature and direction of this evolution.

The Evolution and Increasing Diversity of Japanese Corporations

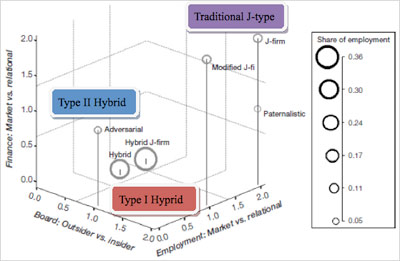

Against a backdrop of globalization and deregulation, Japan’s once largely uniform corporate governance system has undergone major changes, giving rise to a lively debate around the question of whether this transformation signifies a convergence on the U.S. model. To shed light on this issue, Jackson and Miyajima (2007) examined changes, picking up the sample firms in 2002 at a time when the corporate reforms following the banking crisis had largely run their course. The study was based on a cluster analysis of 867 firms listed on the 1stt and 2nd Sections of the Tokyo Stock Exchange (TSE). Japanese firms have grown increasingly diverse, but their transformations signify neither a convergence on the U.S. model nor a continuation of the traditional system. Instead, they are opting for hybrid approaches which combine the two different modes of a market-based system and a relationship-based system.

The results of our analysis are neatly summarized in the Figure. Firms which cluster at 0 on the vertical Finance axis rely to a greater extent on the capital market, and have a higher degree of the outside ownership, while those firms which locate at 2 rely to a greater extent on bank loans and have a larger degree of inside ownership (banks and corporations). Firms that locate at 0 along the Board axis have greater organizational separation of ownership and management, and are more apt to appoint outside directors, and to emphasize information disclosure; while firms that locate at 2 are more likely to have insider directors, and are more reluctant to disclose information. On the Employment axis, firms that cluster at 0 rely to a greater extent on explicit contract-based employment systems that stress fixed terms of employment, performance-based pay schemes, and stock options; while those that are at 2 rely to a greater extent on unwritten long-term employment contracts, and wage systems that have a high correlation with years worked (i.e. seniority-based wages). The relative sizes of the circles in the Figure indicate the relative shares of the workforce of each cluster.

If the traditional Japanese model were still dominant, we would expect a large circle in the region occupied by J-firms (upper right-hand corner). On the other hand, if Japanese corporations have shifted toward the U.S. model from the late 1990s, we would expect a larger circle in the bottom left-hand corner (with values at 0 on all three axes). Instead, however, our analysis reveals that Japanese corporations have grown remarkably diverse in their corporate governance practices, forming distinct sub-clusters which can be broadly combined into three clusters.

The first cluster (Type I Hybrid) is comprised of corporations which combine two different modes – market-based financing and long-term employment practices. These firms (which include Toyota and Canon) have made attempts to modify the long-term employment practices, while also taking active steps to reform their boards. Only 23% of all firms fall into the Type I Hybrid category, but they account for 67% of total employment. They earn comparatively high profits and occupy a predominant position among Japanese firms.

The second cluster (Type II Hybrid) is comprised of firms that have managed to combine relational financing and market-based employment practices. They are, in other words, the inverse of Type I Hybrid firms. Most of these firms are newly established and led by founders. They account for 21% of all firms, and 10% of total employment, and also record relatively high levels of performance.

The third cluster encompasses traditional Japanese firms that combine relational financing with long-term employment practices. Although included within this cluster are the listed subsidiaries and family-run corporations that are either debt-free or have low levels of debt (the Paternalistic and Modified-J-firm sub-clusters in the Figure), most firms in this cluster rely on banks for financing, have inside ownership, fill their boards with insider directors, and offer lifetime employment– in short, the firms in this category conform to the idealized image of traditional Japanese corporations. In 2002, such firms accounted for 26% of all firms, and 11% of the workforce.

Starting at those understanding, I will address how the global financial crisis may impact the evolution of corporate governance arrangements among these firms.

The Reconfiguring of Governance for Traditional Japanese Corporations

Of the three clusters, the cluster that includes traditional Japanese corporations has been dealt the harshest blow by the recent global turmoil. Rapid sales declines have brought the problems posed by their excessive levels of debt to the fore, and forced these firms to take active steps to restructure. Their corporate governance systems are expected to evolve in the following two ways.

First, the government and government-affiliated financial institutions will assume a greater role in their corporate governance. Corporations whose excessive levels of borrowing emerged as a problem during the recession that followed the banking crisis of 1997 finally implemented restructuring measures from 2003 by pursuing mergers and acquisitions and by undertaking other public and private initiatives. But reform proceeded slowly, and economic recovery allowed them to postpone many necessary measures. In fact, some corporations never followed through with debt reduction efforts and thus continue to maintain high levels of debt. As megabanks grew more discriminating in their selection of clients, some firms were kept afloat by loans from regional banks and government-affiliated financial institutions. Recent JAL is the representative of the later case. The recent crisis has brought additional pressure to bear on these firms, and the government is expected to play a key role in their future restructuring plans.

Second, the recent crisis may allow the banking sector to once again emerge as the bedrock of Japanese corporate governance. Since the inside ownership was dominated in this cluster, banks, which have accumulated information on their clients through long-term relationships, are poised to reassert their monitoring roles. Since the early 2000s, a realignment of the banking sector has been underway, leading to the rise to megabanks, and the widespread adoption of internal controls. The megabanks had nearly completely recovered their financial health by disposing non-performing loan around 2004, and were well placed to shoulder the responsibility of governing corporations once again. In the wake of the current crisis, the banks will be expected to pull the trigger to oust managers when the need arises, and to take the initiative in developing restructuring plans.

However, in order to begin assuming governance responsibilities again, banks will have to meet at least two conditions. First, as long as the production of private information is considered to be their strong suit, banks will have to take steps to ensure the quality of their screening efforts. In the 1990s, banks were preoccupied with non-performing loans and were remiss in training adequate screening skills to their loan officers. Over the next few years, it will be essential for banks to improve better screening skills.

Second, banks will have to tie up with buyout funds and consulting companies. In the post-crisis environment, restructuring corporations that face financial hardship will present numerous challenges. Banks have accumulated the know-how to improve balance sheets through asset sales and cost-cutting, but do not have the capacity to devise plans and new business models that will ensure the creation of new corporate value. Hence, banks that seek to turn client companies around will inevitably have to enter into alliances and agreements with buyout funds and consulting companies that can provide the needed expertise.

Redesigning governance for Type II Hybrids as New Companies

Companies that actively adopted fixed-term employment schemes, performance-based wages, and stock options began to appear for the first time in Japan in the late 1990s, and helped to lend a fresh face to the Japanese business community. Since 1999, new IPO markets such as Mothers, JASDAQ, and Heracles have helped to spawn start-up firms in IT-related fields, distribution, and the services industry. Despite their prominence in the media, these new firms still account for only a tiny fraction of the Japanese economy. According to Brown et al. (2009), between 1998 to 2006, which encompasses the dotcom boom, young firms (publicly traded for less than 15 years) accounted for a 40 to 45 percent share of aggregate R&D investment in U.S. research intensive industries. While equivalent young firms in Japan have been increasing their aggregate share of R&D investment in research intensive industries, they still account for less than 5 percent of such investment, and Japan has yet to spawn a corporation comparable to Microsoft or Google. The current crisis has dealt a blow that is primarily financial in nature to the Type II Hybrids, and impacts two aspects of the evolution of their corporate governance arrangements.

First, the crisis has forced Type II Hybrids to reconfigure their financial strategies because they are finding it difficult to raise funds in capital markets. The new IPO markets have contracted rapidly largely because the entrepreneurs/founders of new companies have not been able to inspire confidence in their corporate governance abilities. These entrepreneurs have behaved recklessly, have not disclosed information promptly, and have failed to impose internal systems of control. Unless the corporate governance of these new corporations improves by introducing an adequate regulations, market participants will continue to view them with a jaundiced eye, choking off the possibility that the new IPO markets will reclaim their previous status.

Second, over the longer term, the financial crisis may shape the overall strategies of Type II Hybrids. Although these firms have adopted market-based approaches to employment and compensation, their external governance is not entirely market-based, so their future will be determined by the interplay of two opposing modes or principles. One scenario is that, as corporate finance evolves in a more market-oriented direction, Type II Hybrid employment practices could permeate the entire economy. The other one is that firms in this category may continue to cling to relational-based financing and employment practices gradually converged on relation based one. The current crisis has at the very least reduced the likelihood of the first scenario gaining traction over the short run. Contrary to the understanding that capital markets are the generally preferred venue for raising funds in the risky IT-related industry, in Japan, bank lending has played an important role even for start-ups. The stagnation of new IPO markets during the financial crisis has further amplified the importance of bank lending. Indeed, increasing bank involvement is also expected to help improve the corporate governance of new firms.

Fine-tuning the Governance Arrangements for Type I Hybrids

Type I Hybrid firms sustained the export-led recovery from 2002 to 2007, and have come to play a central role in innovation and to occupy a predominant position among listed firms.

The current crisis has brought considerable suffering to these firms, however, and will influence the evolution of their corporate governance arrangements in two important ways. First, it has put the reconfiguration of the governance of their internal organizations on the front burner. During the recovery that started around 2003, these firms advanced overseas by actively adopting M&A strategies, and achieved growth by setting up holding companies and expanding their corporate groups. The corporate group strategy aimed to reap economies of scale and scope by maintaining lifetime employment even as individual firms within the group implemented their wage systems flexibly. In 2006, 43 of the 500 largest corporations had adopted holding companies, and for firms listed on the First Section of the TSE (excluding holding companies), their consolidated to non-consolidated sales ratio rose from 1.25 in 1993 to 1.70 in 2006. Consequently, within such corporate groups, along with efforts to ensure that managers and outside investors are on the same page, cooperation between holding companies and subsidiaries, and between headquarters and divisions has assumed increasing importance as a corporate governance issue. These groups have been hit hard by the financial crisis, and the decline in demand will force them to reconsider their group business portfolios and to redesign their systems of internal controls.

Second, Type I Hybrids will also have to take steps to manage their relations with outside investors after the crisis abates. These firms depend on the discipline of capital markets including the exercise of voting rights by institutional investors, even as they attempt to maintain their lifetime employment systems. Because Type I Hybrids integrate two opposing business approaches or modes, the inherent tensions contradictions could present challenges that turn into sources of instability.

(1) On the one hand, corporate boards that are controlled exclusively by insiders can be expected to utilize long-term relationships to smoothly manage internal organizational. But outside investors may not be comfortable with the lack of transparency, and control by insiders could mean that insider interests will be excessively privileged. Introducing outsiders directors might be one means of mitigating this problem, but Japan’s market for outside managers is underdeveloped, and the number of people who could serve as suitable outside directors is probably quite limited.

(2) On the other hand, insiders in corporations with employment systems based on long-term relationships might view the raising of funds on capital markets as a potential source of instability because it is tied to external forms of governance. When institutional investors acquire ownership stakes of greater than 50%, and then receive buyout offers with a sufficient premium guaranteed (market experts report that such premiums are usually set at around 35% of the share price), they are highly likely to accept such offers, even when they may not enhance the future value of the corporation. But if corporations adopt takeover defenses to diminish such threats, the likelihood of insider control also increases.

Against the backdrop of stock market crashes triggered by the global financial crisis, overseas institutional investors, prompted primarily by financial concerns, have sold off shares in Type I Hybrid firms, amplifying the decline in their share prices. As the Type I Hybrids experience wild gyrations in their share prices, they will face an important decision with regard to their choice of approach to corporate governance: whether to continue to introduce outsiders to their boards and to implement other board reforms in order to converge on the American model, or to resort once again to practices that will help stabilize shareholding.

Future of Corporate Governance in Japan

Global financial crisis has major impact on the evolution of corporate governance in Japan. The institutions that were drivers of changes from insider system to outside system in corporate governance for a decade (institutional investors, hedge funds, private equity) may not continue to be so. Three points are to be noted as major changes after crisis.

First, the role of government increased: taking an initiative for corporate restructuring, and giving loan guarantee for traditional J-firms, enhanced regulation on new capital market for type II hybrid, and public sector holdings of equity for type I hybrid. Contrary to common perceptions, it may prove much harder to reverse such state interventions. Secondly, the role of bank would be seriously considered for redesigning the corporate finance and governance after crisis: the bank is expected to be an important monitor for the traditional J-firm, and bank finance would be adequate resources for type II hybrid (new firms). The new relational bank would be established, taking much more explicit contracts with clients than former main bank system did. Lastly, the inside ownership will revive with certain level among type I firms. The role of corporate and employee holding of equity should be given serious consideration as alternatives to public and bank ownership.

All happened in Japan is discontinuous changes from pre-crisis. Probably, the landscape of corporate governance in the after crisis may look very different from the pre-crisis.

Increasing Diversity of Corporate Governannce in Japan

– Colloque Penser la crise. De l’intérêt d’une perspective franco-japonaise.

Bibliography :

Jackson, G. and H. Miyajima (2007), “Introduction: The Diversity and Change of Corporate Governance in Japan”, in Aoki, M., G. Jackson and H. Miyajima, eds. (2007). Corporate Governance in Japan: Institutional Change and Organizational Diversity. Oxford University Press, pp. 1-47.

Brown, J., S. Fazzari, and B. Petersen (2009), “Financing Innovation and Growth: Cash Flow, External Equity, and the 1990s R&D Boom.” The Journal of Finance, Vol. 64, pp. 151-185.

Sign up and receive our weekly newsletter for free:

To quote this article :

Hideaki Miyajima, « The Global Financial Crisis and the Evolution of Corporate Governance in Japan »,

Books and Ideas

, 12 November 2009.

ISSN : 2105-3030.

URL : https://booksandideas.net/The-Global-Financial-Crisis-and

Nota Bene:

If you want to discuss this essay further, you can send a proposal to the editorial team (redaction at laviedesidees.fr). We will get back to you as soon as possible.