The explosion of executive pay in recent decades in all Western countries has been the object of considerable criticism. But it has also given rise to an important debate among economists. A recent study by CEPREMAP sums up the various explanations of this phenomenon and suggests some ways in which executive pay could be reformed.

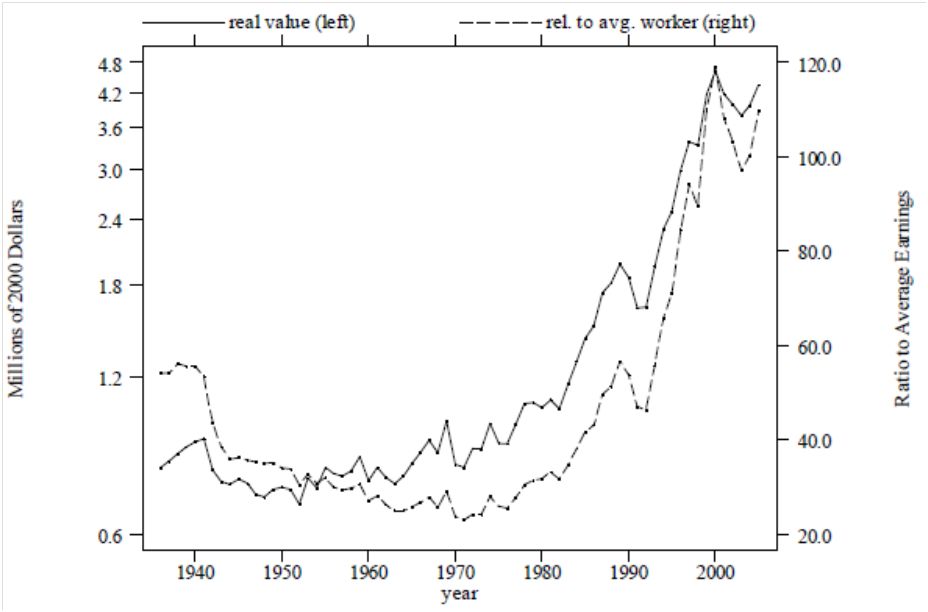

Until the late nineteenth century, family capitalism reigned supreme. It was characterized by small numbers of shareholders, who also ran their own companies. Beginning in the nineteenth century, with the onset of the second industrial revolution, the growth in the size and complexity of the production processes necessitated ever greater investments in companies. Opening company capital to new shareholders became necessary. This growing dispersal of ownership required a new model of corporate leadership. Thus emerged managerial capitalism, in which power and ownership were disconnected: companies were now owned by shareholders, but run by “managers.” Consequently, an optimal way for compensating managers had to be found, both to create incentives to ensure they would act in the shareholders’ best interests and to attract the most qualified candidates. As executive pay rose sharply in the early 1980s, in Europe as well as the United States, the way in which compensation was determined become a topic of academic as well as political debate. Thus Frydman and Saks (2010) show, by studying American executive pay between 1936 and 2005, that while it remained relatively stable through the late 1970s, it subsequently rose at an increasing rate.

Median Value of Compensation Received by the Three Top Positions in the Fifty Largest US Companies Listed on the Stock Exchange (organized into 1940, 1960, and 1990), 1936-2009

Median Value of Compensation Received by the Three Top Positions in the Fifty Largest US Companies Listed on the Stock Exchange (organized into 1940, 1960, and 1990), 1936-2009

In Cepremap’s little book, Comment faut-il payer les patrons (“How Should Executives Be Paid?”), Frédéric Palomino reviews the economic literature on the level and structure of executive compensation. Neither competition for talent nor the implementation of new incentive mechanisms appear to be sufficient to entirely justify increasing pay levels since the late seventies. The question thus becomes: how is pay determined and what limits should be placed on the body that determines them, namely, corporate boards?

Incentivizing Incentive Mechanisms?

The rise in executive pay that began in the 1980s was accompanied by growing consciousness of the importance of incentive mechanisms in the compensation structure. The underlying theory was that of agency (Jensen and Meckling, 1976). When shareholders (the principal) lack sufficient information to control all the decisions made by a CEO (the agent), the compensation structure makes it possible to ensure that the CEO’s interests will line up with those of the shareholders.

Agency Theory

Agency theory belongs to a current of thought that analyzes the effects of incomplete information on economic life. When, in an exchange relationship, the contracting parties do not have the same degree of information, two phenomena result: adverse selection and moral hazard. The latter, which is of particular interest to agency theory, refers to a situation in which one of the contracting parties (the agent) acts on behalf of another (the principal), despite the fact that their interests conflict. If the principal cannot exert complete control over the entirety of the agent’s decisions, the agent cannot act in accordance with the principal’s wishes. Agency theory seeks to define the kind of contract that will ensure that their interests converge. The principal-agent model is evident in different economic situations: between the insurer and the insured, the saver and the bank, and the employee and the employer, as well as between the shareholders and the CEO.

The author discusses the pros and cons of different forms of compensation in terms of incentive: base salary, bonuses, stock options, free shares, and signing bonuses. The use of incentive mechanisms can explain high levels of compensation. Indeed, because executives’ responsibility is limited, insofar as they are not liable if a company fails, shareholders must, when the company is profitable, offer compensation that is as great as the spread between wealth and failure (i.e., the incentive effect) is wide. On balance, when a CEO acts in the shareholder’s interest, she is highly compensated. The incentive mechanisms nonetheless have their limits. In 1990, Jensen and Murphy demonstrated that the responsiveness of executive pay to company performance is relatively weak. If, as Hall and Liebman (2001) have shown, the growing share of stock options and shares in total compensation since the 1990s has increased responsiveness, the variable portion of executive compensation remains much lower in Europe than in the United States. Moreover, stock option value is just as likely to result from external factors and manipulation as from executive performance. Betraind and Mullainathan (2001) thus demonstrate that executive compensation in the oil sector between 1977 and 1994 in the United States was heavily dependent on fluctuations in oil prices over the same period. According to Bebchuk, Grinstein, and Peyer (2011), backdating the date on which stock options are issued also tends to increase their value. Finally, stock option value rises with the volatility of the underlying shares, which can lead executives to take excessive risks to increase their volatility. It is thus not certain that the observed increase in executive compensation since the 1980s is the result of superior executive performance incentives.

Compensation and Competition for Talent

Executive compensation can also be considered the price paid for their talents. According to this theory, companies seek to attract the most competent executives. From this perspective, two factors explain the pay increases since the 1980s: the growing size of companies and increased competition among companies for the same skill sets. First, if one considers that an executive’s talent can increase a company’s value in relation to its size, then the larger a company is, the more likely it is to pay a higher price for greater talent. Gabaix and Landier (2008) show that when there is a market for executives with diverse skill levels, in which the latter are distributed competitively between companies of diverse sizes, then the compensation they receive will grow with median company size. Furthermore, competition is more intense when companies value the same kinds of human capital. Zabojnik (2004) considers that there are two kinds of skills: company-specific skills and general managerial skills. With the development of new information technology and the rise of finance, general skills became increasingly important over the course of the twentieth century. This theory of optimal talent allocation presents, however, a number of problems. First, Terviö (2008) shows that compensation is determined more by distinctive company characteristics, such as size, than it is by scarcity of talent. Moreover, in an article from 2009, he shows that, paradoxically, the more talent has a positive impact on corporate profits, the less executive personnel renews itself and the more likely it is that average talent will be suboptimal. The cost risk of hiring a “novice” does indeed become greater. From this perspective, executive talent has a limited impact on compensation.

The Problem of Corporate Governance

After grasping the limits of theories that explain the structure and level of compensation, one must try to understand why such contracts are offered. The author describes the operation of the corporate board, which is responsible for appointing, supervising, and determining the compensation of the CEO. Her lack of independence vis-à-vis corporate directions is one of the greatest obstacles to effective management. First, the more widely the shareholders are dispersed, the less any one shareholder can exercise oversight and the more a CEO can control her board. The independence of board members is limited by the fact that they often sit on multiple boards. In France, in 2004, 65% of companies listed on the CAC 40 shared at least one board member. Social networks also restrict their independence. Kramarz and Thesmar (2006) show that, in France, the likelihood of being named to a board increases when executives and board candidates belong to the same social networks. In France, executives participate actively in the decisions of the nominating committees that select board members. Also, compensation of board members has little correlation to company performance, as only a small share of it consists of shares. Finally, when corporate boards fulfill their governance tasks poorly and their company is listed on the stock exchange, one might presume that they would be penalized by financial markets. However, the structure of the shareholders community in France appears to limit the threat of takeovers when companies perform poorly.

Proposed Solutions

In 2002, the United Kingdom adopted measures to increase shareholder control over CEO compensation. The procedure, known as “say on pay,” required shareholders to approve CEO compensation each year. Ferri and Maber (2009) show that while these measures had no direct impact on the overall level of compensation, executive concern for performance nonetheless increased.

In the CEPREMAP book, the author proposes three kinds of measures for improving French corporate governance, and, consequently, techniques for determining CEO compensation. First, the independence of corporate boards must be strengthened. The CEO must in no case participate in compensation committees or in the nomination of executives. Furthermore, board member compensation must be linked more strongly to corporate performance, for instance through the use of stock options. Finally, while it is not desirable to put a cap on compensation, tax policy should make it possible to reduce resulting inequalities without modifying executive incentives.

In this book, the author presents the scholarly debate on CEO compensation in a clear and synthetic way. The proposed solutions are very relevant. Because soaring executive compensation is the result not only of dysfunctional governance but also of market forces, it does seem fruitless to place a cap on compensation. As proof, one only has to consider the financial sector, where the regulation of the variable portion of executive pay did not prevent it from reaching new heights in 2010. The author’s analysis seems at times to be somewhat one-dimensional: historical, geographical, and even social considerations tend to be neglected. The issue underlying this debate is not only corporate performance, but also social cohesion, which is threatened by the dramatic rise in inequality. Given the high stakes, greater methodological diversity could enrich the debate.

First published in laviedesidees.fr. Translated from French by Michael C. Behrent with thesupport of the Florence Gould Foundation.

Lucian A. Bebchuk, Yaniv Grinstein, and Urs Peyer. “Lucky CEOs and Lucky Directors.” The Journal of Finance, vol. 65, n°6, 2010, 2363-2400.

Marianne Bertrand and Sendhil Mullhainathan. “Are CEOs Rewarded For Luck? The Ones Without Principals Are.” The Quarterly Journal of Economics, vol. 116, n°3, 2001, 901-932.

Fabrizio Ferri and David Maber. “Say on Pay Vote and CEO Compensation: Evidence from the UK.” Mimeo, Harvard Business School, 2008.

Carola Frydman and Raven E. Saks. “Executive Compensation: A New View for a Long-Term Perspective, 1936-2005.” Review of Financial Studies, vol. 23, 2010, 2099-2138.

Xavier Gabaix and Augustin Landier. “Why Has CEO Pay Increased So Much?.” The Quarterly Journal of Economics, vol. 123, n°1, 2008, 49-100.

Brian J. Hall and Jeffrey B. Liebman. “Are CEOs Really Paid Like Bureaucrats?.” The Quarterly Journal of Economics, vol. 113, n°3, 1998, 653-691.

Michael C. Jensen and Kevin J. Murphy. “Performance Pay and Top-Management Incentives.” The Journal of Political Economy, vol. 98, n°2, 1990, 225-264.

Francis Kramarz and David Thesmar. “Social Networks in the Boardroom.” IZA Discussion Paper Series n°1940, 2006.

Kevin J. Murphy and Jan Zabojnik. “CEO Pay and Appointments: A Market Based Explanation for Recent Trends.” The American Economic Review, vol. 94, n°2, 2004, 192-196.

Marko Terviö. “The Difference That CEOs Make: An Assignment Model Approach.” The American Economic Review, vol. 98, n°3, 2008, 642-668.

Marko Terviö. “Superstars and Mediocrities: Market Failure in the Discovery of Talent.” Review of Economic Studies, vol. 72, n°2, 2009, 829-850.

Sign up and receive our weekly newsletter for free:

To quote this article :

Claire Célérier, « How Should Executives Be Paid? »,

Books and Ideas

, 13 March 2012.

ISSN : 2105-3030.

URL : https://booksandideas.net/How-Should-Executives-Be-Paid

Nota Bene:

If you want to discuss this essay further, you can send a proposal to the editorial team (redaction at laviedesidees.fr). We will get back to you as soon as possible.